Introduction

Since the early 2000s, the oil-rich Gulf Cooperation Council (GCC) member countries underwent two significant economic transformations. The first one was a deliberate policy response to mitigate their heavy reliance on revenue generated from natural resources. A considerable portion of the Gross Domestic Product (GDP) of GCC nations and the bulk of their exports stemmed from income derived from hydrocarbon resources. Recognizing the vulnerabilities associated with such dependency, these countries embarked on efforts to diversify their economies away from oil and gas revenues. The objective was to build resilience against fluctuations in global commodity prices and to channel their resources into sectors promising more sustainable and efficient economic growth.1

In parallel with their domestic diversification initiatives, the second transformation saw GCC countries increasingly seeking to expand their economic influence into other regional economies, such as Egypt, Sudan, Jordan, and Lebanon.2 Leveraging their significant financial resources, they pursued opportunities to establish footholds in business networks across predominantly non-GCC Arab nations in the region. Over the past two decades, the economic significance of the region has grown in the eyes of GCC leaders, reflected in increasing foreign direct investment (FDI) outflows into the region.3 Moreover, the GCC’s growing investment stocks in the Middle East and North Africa (MENA) have rendered the region more attractive for investment flows, bolstering its overall share in global FDI transactions.4

Contemporary research on economic diversification in the Gulf primarily concentrates on the economic and societal impacts of these targeted policies at the domestic level, with limited attention given to the connection between economic diversification policies and the GCC’s geo-economic engagement with the MENA region.5 This study addresses this gap and highlights the link between these two significant economic transformations: the implementation of economic diversification policies and the increasing regional investment outflows of GCC countries to non-GCC Arab countries in the region. Specifically, it examines the trends in investment outflows from two important GCC members, Saudi Arabia and the United Arab Emirates (UAE), to Egypt through a case study approach. By analyzing the prevailing and changing patterns, this study aims to shed light on the relationship between economic diversification efforts within GCC nations and their expanding investment activities in the broader regional context, with Egypt serving as a pertinent case study. The main research questions in this research are: How do the regional investments made by Saudi Arabia and the UAE since the early 2000s reflect their economic statecraft and geopolitical motives? Furthermore, how do these investments align with the economic diversification goals of both nations, and what role do they play in mitigating political, economic, and environmental risks, particularly in the MENA region?

Saudi Arabia and the UAE have long pursued economic diversification efforts, a trend that predates the 21st century. The roots of these endeavors can be traced back to the 1970s when both nations experienced a surge in oil revenues

The study argues that the regional investments allocated by Saudi Arabia and the UAE since the early 2000s serve as a tangible manifestation of their economic statecraft, showcasing their efforts to leverage political power and influence to solidify economic gains outlined in their visions for economic restructuring. This geo-economic strategy aligns with prevailing sectoral trends and investment strategies, particularly evident in the growing FDI outflows from both countries to the MENA region. These investments serve three key functions aligned with Saudi and Emirati political and economic interests: Firstly, they reinforce the material needs of their economic diversification policies by generating revenue in prioritized sectors. Secondly, they enhance their strategic autonomy vis-à-vis other prominent economic and political powers by diversifying investment destinations, thereby reducing political and economic risks associated with concentrating investments in specific regions. Lastly, these regional investments act as a buffer against environmental and climate-related risks, potentially addressing concerns such as food insecurity and the global shift toward green energy by steering investments toward agriculture and renewable energy sectors.

The research elucidates these arguments by analyzing Saudi Arabia and the UAE’s investments in Egypt using two distinct datasets.6 The first dataset comprises shareholder structure data from over 200 companies listed on the Egyptian Stock Exchange between 2009 and 2022. This dataset provides insights into the extent of Saudi and Emirati ownership in these listed firms, along with information on their business characteristics, including their respective sectors. Additionally, this research examined data concerning investments from Saudi Arabia and the UAE into Egypt facilitated by bilateral agreements ranging from 2000 to 2022. Essentially, this data scrutinizes state-sponsored FDI inflows from Saudi Arabia and the UAE into Egypt, analyzing established business ventures and collaborative economic projects resulting from mutual agreements between the governments of Saudi Arabia, the UAE, and Egypt. By utilizing exploratory data analysis strategies and triangulating insights derived from the analyses of these data sources, the research highlights the geo-economics bridge between the economic diversification policies of these nations and their restless economic rapprochement with the MENA region through investment flows.

Economic Diversification in Saudi Arabia and the UAE

Saudi Arabia and the UAE have long pursued economic diversification efforts, a trend that predates the 21st century. The roots of these endeavors can be traced back to the 1970s when both nations experienced a surge in oil revenues. This period coincided with the Yom Kippur War, during which Western nations’ support for Israel prompted the Organization of the Petroleum Exporting Countries (OPEC) to curtail oil production, leading to a sharp increase in oil prices. This windfall of income enriched oil-exporting countries, providing significant resources for reinvestment in their development. Capitalizing on this burgeoning wealth, leaders in Saudi Arabia and the UAE initiated policies aimed at reducing their reliance on oil revenues and diversifying their economies.

The diversification strategy pursued by policymakers involves not only improving the total factor productivity of the private sector but also strengthening the private sector’s capabilities and enhancing its attractiveness by offering competitive wages relative to the public sector

In this initial phase of economic diversification, Saudi and Emirati initiatives can be characterized by two pillars. Primarily, the restructuring of the domestic economy targeted key industrial sectors crucial for advancing infrastructure development projects within both nations. Within this framework, there was a notable emphasis on establishing specialized business ventures focused on the production of steel, aluminum, and cement.7 Additionally, Saudi and Emirati leaders chose to strengthen the role of their nation’s sovereign wealth funds (SWFs) as significant international economic players. Empowered by the steady influx of oil revenues, these SWFs actively sought profitable investment opportunities in developed countries. These economic institutions engaged in purchasing equities and participating in mergers and acquisitions (M&E) with foreign partners. Moreover, alongside direct and portfolio investments in developed nations, Saudi Arabia and the UAE directed their oil surplus into the bond markets of these countries, emerging as crucial sources of finance for Western business ventures.8

The second wave of economic diversification policies commenced in the early 2000s. The Saudi and Emirati governments set out to reduce the overwhelming reliance on oil revenues in their countries’ total domestic production, exports, and government revenues. This was to be achieved by strategically bolstering domestic sectors where Saudi Arabia and the UAE possessed a comparative advantage.9 These early diversification endeavors coincided with a period marked by a surge in oil prices following the Second Gulf War in 2003. Prices continued to climb until their eventual decline after the 2008 financial crisis. The increasing oil prices heralded a considerable flow of revenues into Saudi and Emirati treasuries, granting great opportunities to these countries to reinforce their diversification efforts.10

Two important economic concerns are weighted in Saudi and Emirati calculations to embark on a path of economic diversification. First, the volatility of crude oil prices has been one of the significant financial grievances of these nations.11 The exogenous nature of the fluctuations in oil prices renders the estimation of the projected incoming revenues an extremely laborious task and undermines the reliability of long-term economic development plans based on these estimations.12 Hence, diminishing the reliance on oil has emerged as a pivotal policy measure to mitigate these fluctuations. Secondly, the global push toward the exploration and dissemination of renewable energy sources, coupled with forecasts of the eventual end of the oil age, swayed Saudi and Emirati leaders to invest in sectors potentially conducive to economic growth.13 The anticipation that knowledge-based economic sectors would supersede heavy industries in spearheading economic growth in the post-oil era served as a significant impetus for Saudi Arabia and the UAE to realign their economic priorities.14

The link between Saudi Arabia and the UAE’s regional investments and their efforts to restructure their domestic economies became increasingly apparent with the launch of economic diversification policies in the 2000s

These concerns and strategies for policy action were articulated in the official “vision” documents of these countries. Saudi Arabia unveiled its blueprint for economic diversification with its “Vision 2030” in 2016, while the UAE introduced its “Vision 2021” in 2010.15 In these documents, several sectors were designated as strategic investment targets in which Saudi Arabia and the UAE have comparative advantages. Alongside industrial cycles specialized in the production of steel, aluminum, petrochemicals, cement, and other construction materials, Saudi and Emirati leaders discovered the potential of the service sector.16 Most importantly, Saudi and Emirati leaders have placed significant emphasis on investments in the financial sector, recognizing the comparative advantage of their countries in establishing and developing both bank and non-bank financial institutions.17 Moreover, exploiting the investment opportunities in the touristic recreational facilities has occupied a substantial place in the diversification agendas of the nations.18 The UAE, in particular, has allocated investments toward hotel development, real estate, and land reclamation projects both domestically and regionally. This effort aims to position the UAE as a central tourism hub while establishing the country as a significant investor in the recreational industry across the MENA region.19 In addition to tourism, the UAE has made significant strides in investing in commercial aviation. Recognizing it as pivotal for economic transformation and complementary to tourism, the UAE has worked to establish renowned brands in commercial airline transportation.20

In these new sectoral investments, policymakers aimed to bolster the role of the private sector and provided various incentives to encourage private entrepreneurship.21 Nonetheless, the intention to reinforce the role of the private sector in economic growth did not necessarily undermine the economic initiatives undertaken by the state. Saudis and Emiratis readily leveraged the vast resources accumulated in their SWFs to invest in the essential sectors of their economic diversification schemes while, in the process, creating positive economic externalities for the private sector.22 Similarly, public investments in the financial sector and educational services were intended to bolster the private sector’s access to readily available capital and highly qualified labor. This would ensure that private entrepreneurs do not face shortages in factors of production.23

Another reason for empowering the private sector is to boost employment opportunities for Saudi and Emirati nationals. Despite the substantial increase in wealth among the nationals due to windfall oil revenues, these countries have managed to avoid the detrimental effects of oil wealth overshadowing the private sector’s specialization in tradable goods production (an economic phenomenon known as Dutch Disease).24 The redistribution of oil wealth to nationals hasn’t led to a significant rise in private sector salary levels, potentially increasing production costs and diminishing competitiveness, given the prevalence of expatriate labor willing to work for lower wages in these countries’ private sector.25 Consequently, Saudi and Emirati nationals are more inclined to seek employment in the public sector, which typically offers better wages compared to the private sector. However, the significant number of public sector employees (eg. 67 percent in Saudi Arabia, 81 percent in Qatar)26 poses financial burdens on the treasuries of these countries, limiting their ability to allocate public expenditures efficiently. Therefore, the diversification strategy pursued by policymakers involves not only improving the total factor productivity of the private sector but also strengthening the private sector’s capabilities and enhancing its attractiveness by offering competitive wages relative to the public sector.27 By doing so, Saudi Arabia and the UAE aim to increase the proportion of their workforce employed in the private sector. This policy objective hinges on improving the skills and competencies of nationals in the workforce. Consequently, Saudi and Emirati leaders also implement policies to incentivize and facilitate their citizens’ access to job training necessary for positions requiring high skills and competence.

Investors affiliated with the royal and prominent families of Saudi Arabia and the UAE played a significant role in directing investments to these priority sectors, as well as guiding other investors to discover lucrative business opportunities in the country

Saudi and Emirati Pivot to MENA through Investments

GCC-oriented investors’ pivot to the MENA region has quickly become effective. Between 2003 and 2008, approximately 13 percent of the outflows of GCC countries comprised investments and capital transfers to the countries within the region.28 These investment inflows significantly influenced the FDI portfolios of regional countries in global comparisons. Despite the MENA region’s share in total global FDI flows being less than 1 percent in the early 2000s, this figure surged to 3 percent in the subsequent years thanks to the rising direct investments from GCC countries.29 A substantial amount of these investments targeted developing non-GCC Arab countries such as Egypt, Tunisia, and Jordan.30 Saudi and Emirati investors played a substantial role in boosting the GCC’s investment stock in the MENA region, whose investments exceeded total Western-oriented investments in certain countries.31

The link between Saudi Arabia and the UAE’s regional investments and their efforts to restructure their domestic economies became increasingly apparent with the launch of economic diversification policies in the 2000s.32 Saudi Arabia and the UAE’s inclination to discover investment opportunities in the MENA represents not only a diversification of the location of the investment inflows but also corresponds to a perennial shift in the instrument of these countries’ international investments. Greenfield investments and strategic asset acquisitions have become more important, indicating Saudi and Emirati economic statecraft embedded in planning and undertaking overseas investment policies.33 Three crucial geo-economic processes may account for the Saudi and Emirati pivot to the MENA region in expediting investments.

First, regional investments may function as a gateway for strategic autonomy for Saudi Arabia and the UAE, relieving accumulated political and economic risks of concentrating their investments in merely Western nations. Saudi and Emirati investors’ search for new markets in non-Western countries for allocating investment can be attributed to the political and economic landscape that evolved in the early 2000s. The increasing political concerns in Western countries regarding the geopolitical and geo-economic implications associated with incoming investment flows from non-Western countries, along with the negative economic repercussions stemming from the strained U.S.-GCC relations following the 9/11 terrorist attacks, have heightened Saudi and Emirati considerations of political risk in their investments in the West.34 This has led to a prevailing atmosphere of mutual distrust and discontent, incentivizing Saudi and Emirati investors to hedge some portion of their investments in non-Western markets, such as China, India, and Egypt.35 Additionally, the 2007-2008 financial crisis exacerbated the investment climate in Western countries, eroding trust in the resilience of financial markets. As the crisis swept through Western nations, causing economic turmoil and leaving behind a trail of bankrupted financial institutions and investment funds, it reinforced the Saudi and Emirati perception that solely investing in bonds and equities in Western nations might not be the most prudent choice due to their susceptibility to external economic shocks. This standpoint strengthened the Saudi and Emirati push for diversifying their investment locations, as evidenced by their exploration of investment opportunities in non-Western countries.

The increase in Saudi and Emirati investment in Egypt did not follow a strictly linear pattern, as the pace of investment slowed after the Arab Uprising which led to Mubarak’s removal from power

Second, global policy responses to the problems stemming from climate change solidified the geo-economic linkage between the Saudi and Emirati diversification drive in the domestic landscape and their regional investment trends. Increasing international pledges to reduce carbon emissions and policymakers’ commitment to switching to green energy resources in the foreseeable future boosted the significance of renewable energy investments. This global transition incentivized Saudi and Emirati policymakers to adopt new state-led investment strategies beyond traditional evaluations of bond and equity markets and discover investment potential in the renewable energy sector.36 Particularly in the last decade, Saudi and Emirati green energy investments gained momentum at domestic as well as regional levels thanks to merger and acquisition strategies aimed at acquiring controlling shares of the strategically important energy firms and evincing more cooperation with the local public and private business agents in the region to partake in joint investment projects for constructing and operating renewable energy facilities.37 One of the geo-economic implications of this green energy investment push is that improving the export capacity of renewable energy resources acts as a bulwark against unpredictable fluctuations in hydrocarbon energy exports, and can hedge against the possibility of radical carbon reduction regimes that may emerge as the climate crisis worsens.38 In addition, this hedging strategy may have been conducive to reducing domestic political risks arising from rising budget deficits that may occur at the lower end of oil price fluctuations.39

Finally, environmental pressures emanating from Saudi Arabia and the UAE prompted policymakers to formulate sustainable policies aimed at reducing these countries’ reliance on agricultural imports.40 This underscored the significance of regional agricultural investment and its vital connection to food security. The scarcity of water resources and the ineffectiveness of the prevailing methods to sustain irrigated agriculture compelled Saudis and Emiratis to incentivize agricultural investments in the regional countries. These investments were strategic in a certain aspect. Saudi and Emirati policymakers estimated that regional agricultural investments would secure the sustainability of the agricultural imports that are crucial for the long-term food security of these nations.41 Since subsidiaries of Saudi and Emirati firms are more likely to re-export some portion of the produced goods to Saudi Arabia or the UAE, these countries would be more likely to be hedged by the political risks stemming from geopolitical tensions or geo-economic rivalries.42 Public business entities such as state-owned enterprises and sovereign wealth funds, as well as the business ventures owned by the ruling families and prominent business elites of these nations, soared their regional agricultural investments, pinpointing the strategic importance of these regional agricultural investments.43

In sum, Saudi and Emirati regional investments can be conceived in a geo-economic policy framework, potentially advancing the sectoral development objectives outlined in their diversification plans, and mitigating political risks arising from over-concentration of investments in specific regions and addressing environmental concerns such as food security and the global trend toward green energy, particularly accelerated by events like the Russia-Ukraine war. The following section examines the geo-economic impact of Saudi and Emirati investment outflows in Egypt, the most important destination of GCC-oriented investment flows.44 The section highlights the link between these investments and the broader economic restructuring efforts of Saudi Arabia and the UAE, as well as identifies converging and diverging trends of these investments in the Egyptian context.

Saudi and Emirati Investments in Egypt

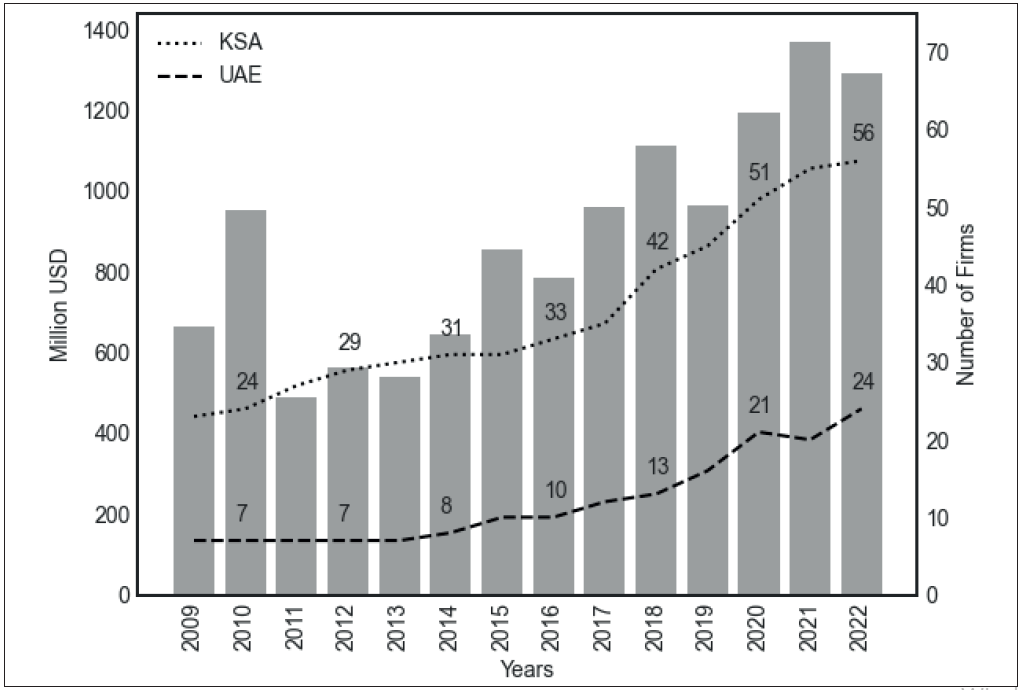

Over the past 20 years, the interest of Saudi and Emirati investors to evaluate business opportunities in Egypt has grown. In 2001, Saudi and Emirati investors invested in about 600 projects.45 In the following 17 years, the number of companies invested in Saudi and Emirati companies increased to 6,000, indicating the growing economic importance of Egypt to Saudi and Emirati investors.46 This increase can also be seen on the Egyptian Stock Exchange (EGX). Figure 1 shows the number of Egyptian firms listed on the EGX that have received significant investment from either Saudi or Emirati investors. The number of firms with Saudi and Emirati investment has gradually increased over the years observed.

The real estate, tourism, financial, and agricultural sectors attracted the bulk of Saudi and Emirati investment in Egypt in the early 2000s. Investors affiliated with the royal and prominent families of Saudi Arabia and the UAE played a significant role in directing investments to these priority sectors, as well as guiding other investors to discover lucrative business opportunities in the country. Saudi Prince Al Waleed Bin Talal Al Saud and the Saudi Bin Laden Group led investments in the tourism and real estate sectors,47 either establishing or acquiring hotel and leisure facilities around Egypt’s tourist hot spots, such as Alexandria and Sharm El-Sheikh. The UAE-based Emaar Properties and Burooj Properties also invested in the tourism sector, focusing on projects around Sidi Abdel-Rahman and Six of October City.48

Hosni Mubarak’s policy of overhauling Egypt’s business environment through legal reforms and the introduction of new incentives and exemptions to attract foreign investors was particularly conducive to attracting Saudi and Emirati investment to Egypt.49 Mubarak primarily targeted Gulf investors to play a role in his economic liberalization policies, attempting to persuade them to participate in business projects announced under the public-private partnership program, which calls for greater cooperation between private investors and publicly owned companies.50

However, the increase in Saudi and Emirati investment in Egypt did not follow a strictly linear pattern, as the pace of investment slowed after the Arab Uprising which led to Mubarak’s removal from power. As can be seen in Figure 1, new investments seem to have stagnated during the term of Mohamed Morsi, whose tenure was not welcomed by the Saudi and Emirati leaders. Investment trends, both in terms of the number of companies and the total investment value of Saudi and Emirati capital, recovered after the 2013 military coup that toppled Morsi and paved the way for the presidency of Abdel Fattah el-Sisi, who managed to gain tangible political and economic support from the Saudi and Emirati regimes to consolidate his power. Figure 1 shows that the increasing investment appetite of Egypt’s Saudi and Emirati partners during Sisi’s presidency can be more easily observed in terms of new UAE-originated investments allocated to Egyptian firms, as the number of firms with Emirati investments appears to have tripled since Sisi came to power following the 2013 military coup.

Figure 1: The Count of Egyptian Firms in EGX with Saudi and Emirati Investment and Their Total Stock Value (US Dollars Adjusted to 1983 Prices)

Source: Prepared by the Author

Sisi’s rise to power coincides with a rush of investment from Saudi Arabia and the UAE, modulated by an observable political drive. In 2016, Saudi Arabia signed a memorandum of understanding (MoU) with Egypt to establish a joint investment fund with a capital of $16 billion. The Saudi Public Investment Fund would be responsible for financing projects carried out by the joint venture established in Egypt.51 The MoU was signed during the Saudi king’s unusually long visit to Egypt, and the agreement was followed by other investment agreements, most notably the allocation of about 2020 km2 of agricultural land to Saudi businessmen.52 After Saudi Arabia’s new business agreements concluded during the Saudi king’s visit, the UAE followed the footprint of Saudi economic statecraft in Egypt. Shortly after Saudi Arabia’s high-level deals with Egypt, the UAE’s Mohamed Bin Zayed Al Nahyan visited Cairo and conveyed the Emirati interest in participating in Egypt’s state-led project to build the New Administrative Capital, as well as signing a MoU to establish a joint investment company whose Emirati shares will be capitalized by one of the UAE’s leading sovereign wealth funds, Abu Dhabi Developmental Holding Company (ADQ).53

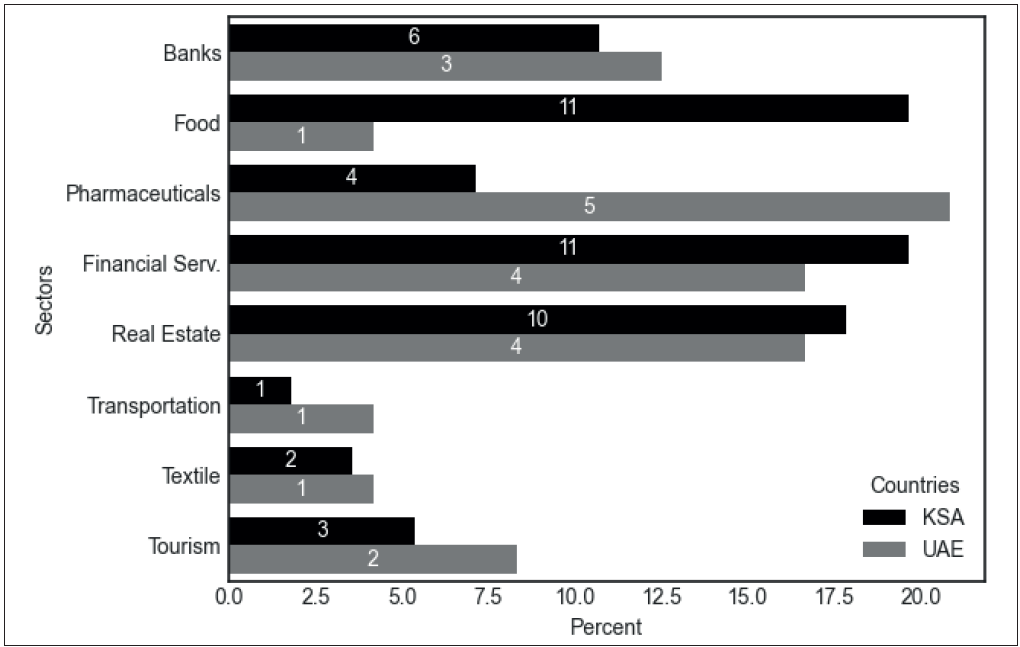

Figure 2: The Sectoral Distribution of Egyptian Firms Listed on EGX with Significant Investments from Saudi Arabia or the UAE in 2022

Source: Prepared by the Author

Sectoral analysis of Saudi and Emirati investments in Egyptian companies listed on the stock exchange can shed light on the divergences and convergences of the sectoral predisposition of FDI. Figure 2 shows the distribution of the Egyptian companies listed on the stock exchange that have significant Saudi or Emirati investments in certain selected sectors. The bars show the percentages of the total Emirati and Saudi firms operating in the designated sector, and the number on the bars shows the number of Saudi or Emirati-invested domestic firms in the referred sector. The banking and non-banking financial services sectors are among the key business areas where Saudi and Emirati investment trends converge. Saudi and Emirati investors have a visible presence in the Egyptian financial sector, holding significant stakes in local Egyptian banks. In addition, Saudis and Emiratis hold controlling stakes in some of the largest financial institutions, gaining exclusive management authority. For example, the Faisal Islamic Bank of Egypt was founded in 1977 by Mohammed bin Faisal Al Saud as a Sharia-compliant joint stock company. In addition, another Islamic financial institution, al-Baraka Bank Egypt, was established as a subsidiary of the multinational al-Baraka Banking Group, headquartered in Saudi Arabia. Similarly, Abu Dhabi Islamic Bank Egypt is one of the subsidiaries of the UAE’s Abu Dhabi Islamic Bank Egypt, in which the UAE’s state-owned investment arm, the Abu Dhabi Investment Authority, holds substantial controlling stakes.

State-sponsored investments in Saudi Arabia and the UAE indicate that one capital-intensive sector has attracted considerable interest from these countries: renewable energy

Another major sector where Saudi and Emirati investment appetites converge is real estate. Emaar Misr for Development, one of the subsidiaries of the UAE-based multinational Emaar Properties, is a prominent player in the UAE’s real estate investment network in Egypt. Another leading real estate investment company, Six of October Development and Investment (SODIC), was acquired by the UAE’s state-owned Aldar Properties in 2021.54 In line with Saudi and Emirati investors’ exploration of business opportunities in real estate, tourism investments from these countries also show similar trends. Data from the EGX suggests that Saudi and Emirati investors have shown similar interest in building hotels and recreational facilities near Egypt’s tourist hot spots, in an effort to gain a compelling edge in Egypt’s tourism sector. In 2014, the tourism and real estate development sectors had the lion’s share of Saudi and Emirati investments, accounting for about 65 percent of the total FDI stock.55 Subsidiaries of Saudi and Emirati sovereign wealth funds invested in large-scale real estate development projects, as well as state-led and military-sponsored land reclamation projects, which were launched near the Toshka region and the Suez Canal.56

Figure 2 also reveals two key differences in the sectoral preferences of Saudi and Emirati investors in Egyptian listed companies. First, Emirati investors are more inclined to invest in the pharmaceutical and healthcare sectors than Saudi investors. As shown in Figure 3, Emirati investors have placed more emphasis on investing in the healthcare sector in recent years, accounting for a significant share of listed Egyptian companies with Emirati investment. Although Saudi investment in pharmaceuticals is actually present in four listed local firms, this sector plays a more significant role in UAE-originated investment, given the sectoral distribution of local firms attracting a prominent level of UAE investment. This may indicate that Emirati investors are more willing to invest in sectors that require a greater amount of capital devoted to research and development. This finding implies that the UAE may be different from Saudi Arabia and other GCC countries, which invest relatively less in research and development (R&D) despite the presence of large resources at their disposal.57

Saudi and Emirati investments converge with investments in the renewable energy sector in Egypt, demonstrating the common approach of these countries to mitigate the risks associated with global policy responses to climate change

Nevertheless, state-sponsored investments in Saudi Arabia and the UAE indicate that one capital-intensive sector has attracted considerable interest from these countries: renewable energy. Official contacts between the Saudi and Emirati governments culminated in lucrative deals for private and public players in Egypt’s renewable energy sector. To illustrate, Masdar, a subsidiary of the UAE’s sovereign wealth funds, has been involved in several investment ventures in the energy sector. These efforts include projects such as the establishment of green hydrogen production facilities in the Suez Canal Economic Zone and along the Mediterranean coast. In addition, Masdar has committed to working with the Egyptian Renewable Energy Authority to build a wind-powered renewable energy facility.58 Similarly, Saudi Arabia’s ACWA has reached an agreement with the Egyptian government to build solar and wind power plants in the West Nile region.59 These renewable energy investments by Saudi Arabia and the UAE are consistent with their economic diversification visions, which include increasing investment in green energy resources.60 The Saudi and Emirati governments consider the development of renewable energy production capacity as a viable investment strategy because it can be built on existing institutional capacity, infrastructure, and knowledge.61 Moreover, the abundance of available land and solar yields makes green energy production a domain of comparative advantage and a fertile means of diversifying their exports. It can therefore act as a hedge against both annual oil price fluctuations and long-term trends in the world’s transition to renewable energy consumption under the pressure of climate change.62

On the other hand, Saudi investment diverges from the preferences of UAE-origin investors when it comes to funds directed to the food industry. As can also be seen in Figure 3, investment inflows from Saudi Arabia into Egypt’s agricultural sector accelerated after the Arab Uprising, taking a prominent place among Saudis’ sectoral preferences, along with real estate and financial investments. Saudi figures show that Saudi investors show considerable interest in allocating investments to Egypt’s agricultural industries, culminating in agricultural investments representing more than 20 percent of all Egyptian companies with significant Saudi investment. Major Saudi conglomerates have invested in Egypt’s agricultural sector. The Saudi-based Savola and Havani Brothers groups became prominent through their agricultural and livestock investments in Egypt. These investments facilitated their acquisition of a substantial share of the Egyptian domestic market. These companies pursued a strict strategy of vertical integration in the Egyptian market, investing not only in the production of agricultural raw materials but also in securing market power in the supply chain of the agricultural products produced in regional markets.63 Some of the Saudi companies have invested heavily in government-sponsored land reclamation projects, acquiring large tracts of land allocated for cultivation. The underlying irrigation systems and other infrastructure are provided by the Egyptian government, and the investing companies are granted other commercial privileges.64 In addition, Saudi investors have maintained good relations with the Egyptian military in order to gain access to certain land reclamation projects whose entry licenses are strictly regulated by the military institution, such as the land reclamation project initiated in the Sharq El Oweinat region.65

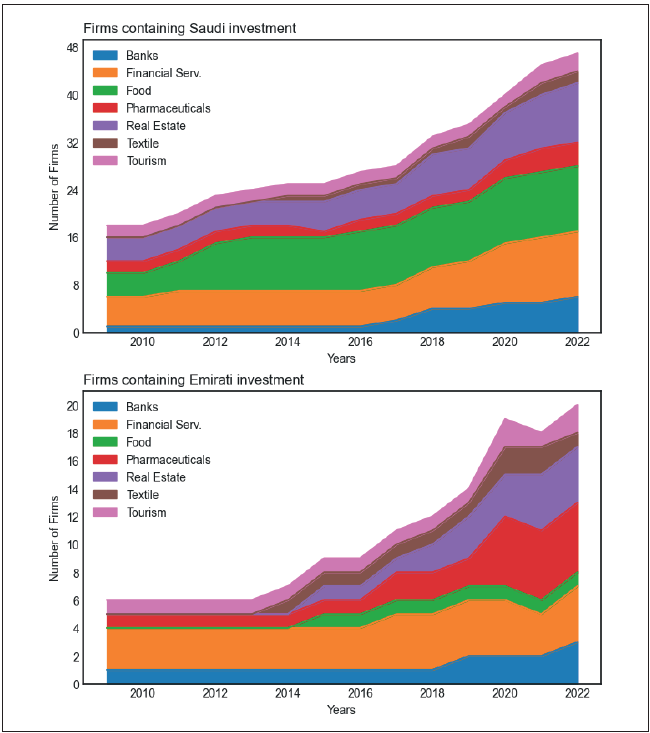

Figure 3: Sectoral Distribution of Egyptian Firms Listed in EGX with over 10 Percent Ownership by Saudi or Emirati Investments between 2009 and 2022.

Source: Prepared by the Author

Conclusion

This article examined the relatively understudied link between GCC member states’ economic diversification policies and these countries’ regional investment flows to non-GCC Arab countries, which have accelerated since the early 2000s. Using a case study design, this study examines Saudi Arabia’s and the UAE’s investment patterns in Egypt and the extent to which these countries’ investment patterns are consistent with their economic statecraft, which includes geo-economic motives. Specifically, this research explores the compatibility of regional investment trends and economic diversification goals and examines how these two economic transformations reinforce each other to contribute to Saudi and Emirati geo-economic policymaking to address political, economic, and environmental risks.

The analysis of the EGX and state-sponsored investment data shows that Saudi Arabia and UAE-originated investments in Egypt have been gradually increasing since the early 2000s, albeit some aberrations occurred due to the changing political landscape following the Arab Uprising. After Saudi Arabia and the UAE’s favored incumbent, Abdel Fattah el-Sisi, came to power, investments from these countries gained unprecedented momentum. Both Saudi and Emirati state-led investment vehicles and conglomerates linked to the political and business elite of these countries had consolidated their foothold in the Egyptian economic landscape, exploring investment opportunities through partnerships with either Egyptian state institutions or prominent local private business actors. Particularly after 2015, subsidiaries of Saudi and Emirati sovereign wealth funds invested in strategic real estate, tourism, agriculture, renewable energy, and financial sectors, either pursuing M&Es or partaking in joint investment companies established in partnership with local public or private actors.

By directing investments toward efficient and productive sectors, it’s possible to address longstanding unemployment challenges, thereby promoting enduring economic stability and self-reliance

The sectoral analysis of these Saudi and Emirati investments shows that the bulk of the investments target sectors that are prioritized in these countries’ economic diversification visions, highlighting the policy link between these countries’ domestic economic restructuring efforts and their regional investment flows. Moreover, Saudi and Emirati investments converge with investments in the renewable energy sector in Egypt, demonstrating the common approach of these countries to mitigate the risks associated with global policy responses to climate change. Nevertheless, Saudi and Emirati investment trends differ when it comes to specific sectors. Saudi Arabia shows more interest in agricultural investments, which could be related to the fact that Saudi Arabia is more concerned about food insecurity due to its larger population. On the other hand, the UAE shows a greater propensity to invest in the capital-intensive pharmaceutical and healthcare sectors, which contrasts with the prevailing trend in the GCC of allocating fewer resources to business ventures that require intensive investment in research and development.66

The study highlights a significant insight: The current investment patterns of Saudi Arabia and the UAE in the MENA region reflect a strategic economic approach. This suggests a deliberate effort by leaders in both countries to utilize political and economic resources to foster greater regional economic integration, with them taking the lead. This growing economic cooperation could offer substantial prospects for sustainable growth and development across the region. By directing investments toward efficient and productive sectors, it’s possible to address longstanding unemployment challenges, thereby promoting enduring economic stability and self-reliance.

However, the research also identifies certain trends that foreshadow future economic challenges for Saudi Arabia, the UAE, and other non-GCC Arab nations. Firstly, data indicates that a significant portion of Saudi and Emirati investments in Egypt are directed toward labor-intensive sectors, potentially reinforcing the rentier nature of regional economies instead of fostering development in capital and technology-driven industries. While the UAE deviates somewhat from Saudi Arabia with its substantial investments in pharmaceuticals, requiring funds for R&D, other sectoral trends are less encouraging. Furthermore, apart from investments in agriculture and pharmaceuticals, the analysis reveals a substantial convergence in sectoral trends between Saudi and Emirati investments in Egypt. This convergence is understandable, given the comparative advantages these countries hold in certain sectors globally. However, such similar sectoral trends might limit the potential for specialization among regional countries and could adversely affect prospects for regional economic integration in the future.

Endnotes

1. Matthew Gray, The Economy of the Gulf States, (Newcastle upon Tyne: Agenda Publishing, 2018); Martin Hvidt, “Economic Diversification in the Gulf Arab States: Lip Service or Actual Implementation of a New Development Model?” in Bessma Momani and Matteo Legrenzi (eds.), Shifting Geo-Economic Power of the Gulf: Oil, Finance and Institutions, (London and New York: Routledge, 2011); Asharf Mishrif, “Introduction to Economic Diversification in the GCC Region,” in Ashraf Mishrif and Yousuf Al Balushi (eds.), Economic Diversification in the Gulf Region, 1, (Palgrave Macmillan, 2017); Bessma Momani, “Shifting Gulf Arab Investments into the Mashreq: Underlying Political Economy Rationales?” in Bessma Momani and Matteo Legrenzi (eds.), Shifting Geo-Economic Power of the Gulf, (London and New York: Routledge, 2011); Mary Ann Tétreault, “Gulf Arab States’ Investment of Oil Revenues,” in Bessma Momani and Matteo Legrenzi (eds.), Shifting Geo-Economic Power of the Gulf, (London and New York: Routledge, 2011); Kristian Ulrichsen, “Economic Diversification in Gulf Cooperation Council (GCC) States,” Center of Energy Studies, (June 2017).

2. Karen E. Young, The Economic Statecraft of the Gulf Arab States, (Bloomsbury Publishing, 2022).

3. Momani “Shifting Gulf Arab Investments into the Mashreq,” p. 168.

4. Adam Hanieh, Capitalism and Class in the Gulf Arab States, (Springer, 2016), p. 150.

5. Sarah Muhanna Al Naimi, “Economic Diversification Trends in the Gulf: The Case of Saudi Arabia,” Circular Economy and Sustainability, Vol. 2, No. 1 (August 28, 2021); Martin Hvidt, “Economic Diversification and Job Creation in the Arab Gulf Countries: Applying a Value Chain Perspective,” in Giacomo Luciani and Tom Moerenhout (eds.), When Can Oil Economies Be Deemed Sustainable, (Springer, 2021); Nazar Hilal, “Tourism in the Gulf Cooperation Council Countries as a Priority for Economic Prospects and Diversification,” Journal of Tourism and Hospitality, Vol. 9, No. 451 (2020); Karen E. Young, “Federal Benefits: How Federalism Encourages Economic Diversification in the United Arab Emirates,” in Martin Beck and Thomas Richter (eds.), Oil and the Political Economy in the Middle East, (Manchester University Press, 2021); Osman Antwi‐Boateng and Noura Hamad Salim Al Jaberi, “The Post‐Oil Strategy of the UAE: An Examination of Diversification Strategies and Challenges,” Politics & Policy, Vol. 50, No. 2 (2022).

6. Ömer Naim Küçük, “Investing in Authoritarianism: Saudi Arabia and the UAE’s FDI Inflows into Egypt under Sisi,” PhD Dissertation, Middle East Technical University, 2024.

7. Martin Hvidt, “Economic Diversification in GCC Countries: Past Record and Future Trends,” RePEc: Research Papers in Economics, (2013).

8. Mehran Kamrava, The Political Economy of Rentierism in the Persian Gulf, (Oxford University Press, 2012); Tétreault, Gulf Arab States’ Investment of Oil Revenues.

9. Hvidt, “Economic Diversification in GCC Countries,” p. 41.

10. Tétreault, Gulf Arab States’ Investment of Oil Revenues.

11. Tim Callen, Reda Cherif, Fuad Hasanov, Amgad Hegazy, and Padamja Khandelwal “Economic Diversification in the GCC: Past, Present, and Future,” IMF Staff Discussion Note, Vol. 14, No. 12 (December 2014).

12. Callen, et al., “Economic Diversification in the GCC.”

13. Robert D. Blackwill and Jennifer M. Harris, War by Other Means, (Harvard University Press, 2016).

14. Kamrava, The Political Economy of Rentierism in the Persian Gulf.

15. “Vision 2021,” United Arab Emirates, retrieved from https://u.ae/-/media/Resources/uae_vision-Eng.ashx.

16. Hvidt, “Economic Diversification in the Gulf Arab States.”

17. Hvidt, “Economic Diversification in GCC Countries”; Ashraf Mishrif and Yousuf Al Balushi, Economic Diversification in the Gulf Region: Comparing Global Challenges, (Springer, 2018).

18. Stephen Grand and Katherine Wolff, “Assessing Saudi Vision 2030: A 2020 Review,” Atlantic Council, retrieved from https://www.atlanticcouncil.org/in-depth-research-reports/report/assessing-saudi-vision-2030-a-2020-review/.

19. Mishrif, Introduction to Economic Diversification in the GCC Region.

20. Hvidt, “Economic Diversification in GCC Countries.”

21. Hvidt, “Economic Diversification in GCC Countries.”

22. Mishrif, Introduction to Economic Diversification in the GCC Region.

23. Hvidt, “Economic Diversification in GCC Countries.”

24. Giacomo Luciani, “Framing the Economic Sustainability of Oil Economies,” in Giacomo Luciani and Tom Moerenhout (eds.), When Can Oil Economies Be Deemed Sustainable?, (Springer, 2021).

25. Callen, et al., “Economic Diversification in the GCC.”

26. Antonio Carvalho, Jeff Youssef, and Nicolas Dunais, “Increasing Private Sector Employment of Nationals in the GCC Labour Policy Options to the Rescue,” Tri International Consulting Group, (2017), pp. 1-15.

27. Callen, et al., “Economic Diversification in the GCC.”

28. Legrenzi, “Shifting Gulf Arab Investments into the Mashreq.”

29. Hanieh, Capitalism and Class in the Gulf Arab States, p. 150.

30. Fred H. Lawson, “The Persian Gulf in the Contemporary International Economy,” in Mehran Kamrava (ed.), The Political Economy of the Persian Gulf, (New York: Columbia University Press, 2012), pp. 19-20.

31. Hanieh, Capitalism and Class in the Gulf Arab States.

32. Rafeef Ziadah, “The Importance of the Saudi-UAE Alliance: Notes on Military Intervention, Aid and Investment,” Conflict, Security & Development, Vol. 19, No. 3 (2019).

33. Milan Babic, Javier Garcia-Bernardo, and Eelke M. Heemskerk, “The Rise of Transnational State Capital: State-Led Foreign Investment in the 21st Century,” Review of International Political Economy, Vol. 27, No. 3 (2020).

34. Ulrichsen, “Economic Diversification in Gulf Cooperation Council (GCC) States.”

35. Tétreault, Gulf Arab States’ Investment of Oil Revenues.

36. Jamil, Farzana Ahmad, and YJ Jeon, “Renewable Energy Technologies Adopted by the UAE: Prospects and Challenges– A Comprehensive Overview,” Renewable and Sustainable Energy Reviews, Vol. 55, (2016).

37. “UAE Support for Egypt Strong Bound to Continue,” MENA English, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:5H24-4K71-F04Y-T0N2-00000-00&context=1516831.

38. Dawud Ansari, “The Hydrogen Ambitions of the Gulf States: Achieving Economic Diversification While Maintaining Power,” SWP Comment, No. 44 (July 2022).

39. Ansari, “The Hydrogen Ambitions of the Gulf States.”

40. Ulrichsen, “Economic Diversification in Gulf Cooperation Council (GCC) States.”

41. Adam Hanieh, Money, Markets, and Monarchies, (Cambridge University Press, 2018).

42. Hanieh, Money, Markets, and Monarchies.

43. Hanieh, Money, Markets, and Monarchies.

44. Ziad Daoud, “Gulf States Learn the Power and Limits of Petrodollar Persuasion,” Bloomberg, (April 24, 2024), retrieved from https://www.bnnbloomberg.ca/gulf-states-learn-the-power-and-limits-of-petrodollar-persuasion-1.2063026.

45. “Saudi Arabia Invests in 563 Egyptian Companies,” IPR Strategic Business Information Database, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:44S4-T2F0-003N-V1XM-00000-00&context=1516831.

46. Shaimaa Raafat, “UAE’s Investments in Egypt to Increase: Ambassador,” Daily News Egypt, (December 1, 2018), retrieved from https://www.dailynewsegypt.com/2018/12/01/uaes-investments-in-egypt-to-increase-ambassador/.

47. “Sarmad N. Zok, Ceo, Kingdom Hotel Investments,” Middle East Company News Wire, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:4H8N-W3R0-TX0W-M2TF-00000-00&context=1516831.

48. “UAE’s Emaar N. Coast Tourist Project Contract,” IPR Strategic Business Information Database, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:4KKG-

FKD0-TX70-H2YM-00000-00&context=1516831.

49. Shima’a Hanafy, “Patterns of Foreign Direct Investment in Egypt: Descriptive Insights from a Novel Panel Dataset at the Governorate Level,” MAGKS Joint Discussion Paper Series in Economics, (2015).

50. “Rachid’s Intensive Talks with UAE Official on Economic Cooperation, Joint Projects,” States News Service, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:51PB-K2C1-JCBF-S4C6-00000-00&context=1516831.

51. “Egypt, Saudi Arabia Agree on $16b Fund, Settle Maritime Spat,” The Times of Israel, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:5JH3-HWR1-JDJN-607J-00000-00&context=1516831.

52. “Egypt to Allocate 500,000 Acres of Arable Lands to Saudi Investors: Saudi Minister,” MENA English, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:5JHH-

GHX1-JDJN-63TY-00000-00&context=1516831.

53. “Egypt, UAE Discuss Cooperation in Real Estate Projects,” Daily News Egypt, retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:5JMY-NS01-F11P-X221-00000-00&context=1516831.

54. “Aldar, Adq Are Now Sodic’s Majority Shareholders,” Enterprise, (December 8, 2021), retrieved from https://enterprise.press/stories/2021/12/08/aldar-adq-are-now-sodics-majority-shareholders-60210/.

55. Abdel Razek Al-Shuwekhi, “$10bn Total UAE Investments in Egypt: Gafi Head,” retrieved from https://advance.lexis.com/api/document?collection=news&id=urn:contentItem:5DPX-8331-F11P-X39T-00000-00&context=1516831.

56. David Prina, “Taking Care of Their Own: The Causes and Consequences of Soldiers in Business,” Business, Political Science, (2017).

57. Mishrif and Al Balushi, Economic Diversification in the Gulf Region.

58. “UAE Support for Egypt Strong Bound to Continue,” MENA English.

59. Mohamed Farag, “Nrea, Acwa Power Sign Mou to Establish Solar, Wind Plants,” Daily News Egypt, (April 10, 2016), retrieved from https://www.dailynewsegypt.com/2016/04/10/nrea-acwa-power-sign-mou-to-establish-solar-wind-plants/.

60. Ansari, “The Hydrogen Ambitions of the Gulf States.”

61. Ansari, “The Hydrogen Ambitions of the Gulf States.”

62. Liath Alajlouni, Amnah Ibraheem, and Asna Wajid, “The Gulf States Push for Renewables but Face Challenges in Climate Diplomacy,” Institute for Strategic Studies (IISS), retrieved from https://www.iiss.org/online-analysis/online-analysis/2023/12/the-gulf-states-push-for-renewables-but-face-challenges-in-climate-diplomacy/.

63. Steffen Hertog, “The GCC and Arab Economic Integration: A New Paradigm,” Middle East Policy, Vol. 14, No. 1 (2007).

64. Christian Henderson, “Gulf Capital and Egypt’s Corporate Food System: A Region in the Third Food Regime,” Review of African Political Economy, Vol. 46, No. 162 (2019).

65. Henderson, “Gulf Capital and Egypt’s Corporate Food System.”

66. Mishrif and Al Balushi, Economic Diversification in the Gulf Region.